More prospective borrowers are resorting to fraud in the face of fewer auto financing options.

Auto financing was harder to come by in November, according to the team over at autoremarketing.com in a recent article (Auto credit tightens in November).

The article referred to the Cox Automotive Dealertrack Auto Credit Availability Index, which accounts for changes in approval rates, subprime shares, yield spreads, and contract details, including term length, negative equity, and down payments, reflects credit access for auto loan borrowers. Shifts in its underlying criteria pointed toward a recent credit crunch, with the Index ticking down to 94.8 in November, a year-over-year decrease of 4.2 percent. Notably, credit unions saw the most tightening among lenders.

This makes for a more difficult time for dealers, with less attractive finance rates putting some consumers off and potentially pushing others to misrepresent their loan application details. Dealers should be aware of the implications this credit environment has on fraud.

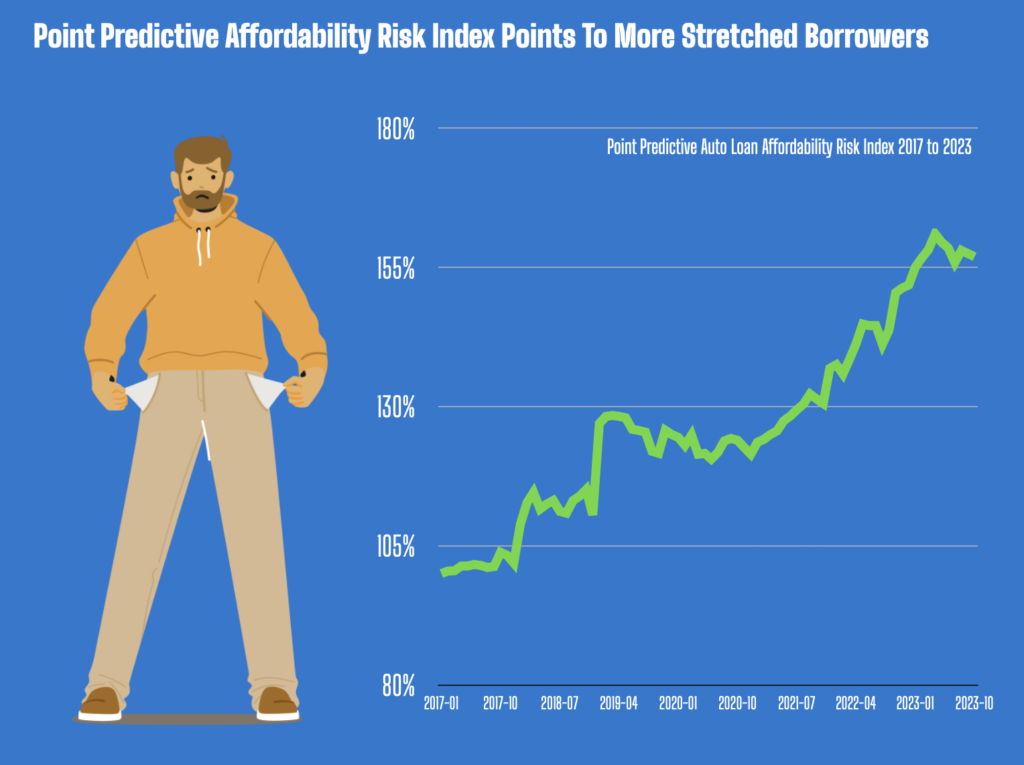

Amid the more restrictive lending environment resulting in more stretched borrowers as shown by the Point Predictive Affordability Index, our fraud analysts also detected a spike in November in synthetic identity fraud, as well as income representation.

The correlation suggests that, as high interest rates affect many of the factors included in the index, more loan applicants are resorting to fraud as they strive to finance auto purchases, particularly in the subprime space and for loans issued by indirect lenders.

Such fraud could take the form of sophisticated operations. As Point Predictive’s Frank McKenna recently explained, one crime ring consists of a team of experienced fraudsters meticulously creating identities and physically delivering vehicles to the end consumer. For a flat fee, customers can outsource the creation of a synthetic identity, complete with a stolen or fabricated social security number and other personally identifiable information. The group’s expertise lies in using credit privacy numbers (CPNs) to construct deceptive applicant profiles, allowing customers to secure favorable financing for vehicles without actively participating in the fraud, though they risk legal consequences and potential involvement in broader criminal activities.

On the other end of the spectrum, fraud could be as simple as an applicant exaggerating their income to increase their likelihood of being approved for a loan or receiving more favorable terms.

Regardless of the method, as credit tightens, the rise in synthetic identities and other fraudulent practices poses a tangible threat to auto dealers and their lending partners, exposing them to heightened risks, such as early payment defaults and buybacks.

Stay Ahead of Fraud with help from Point Predictive

As the effects of tighter credit availability persist and fraudsters adapt their tactics, a proactive and collaborative approach within the automotive financing sector is paramount to preserving the integrity of the lending process and protecting lenders and consumers alike.

Tools like Point Predictive’s BorrowerCheck leverage historical application and loan data, in combination with the nation’s largest data repositories, third-party data, and Point Predictive Consortium data to accurately identify risks associated with applicant-stated identity, income, or employment information.